In today’s financial landscape, borrowing money can serve as a lifeline for achieving personal and professional goals. From consolidating debts to funding home improvements, securing large sums of cash is essential for many Americans. Two primary avenues exist: personal loans and home equity loans. Each has its unique set of advantages and drawbacks, making the decision process akin to choosing between two proverbial apples—one shiny red with a tempting crunch, while the other might be more robust but harder to bite into.

FastLendGo offers a user-friendly platform for comparing loan options, ensuring you make an informed choice that aligns perfectly with your financial needs. Whether you’re considering a personal loan or delving deeper into the world of home equity loans, understanding the nuances can save you from biting off more than you can chew.

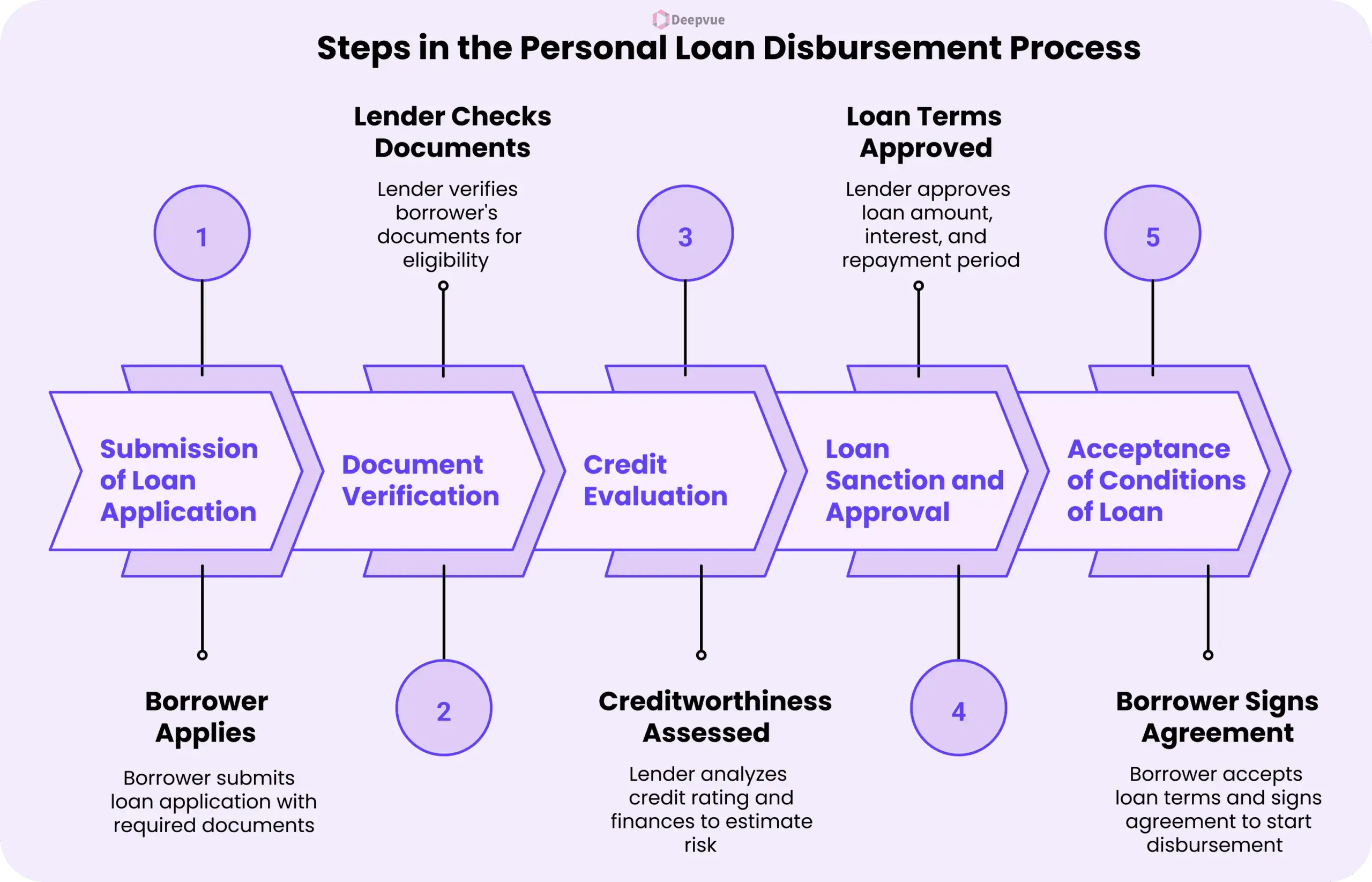

The Sweet and Sour of Personal Loans

Personal loans are unsecured lines of credit that come with their own unique set of benefits and risks. These loans are often used for a variety of purposes, ranging from debt consolidation to funding a dream vacation or making significant home improvements. However, the choice to opt for one depends heavily on your financial situation.

One of the primary advantages of personal loans is their accessibility. With fast approval times and flexible repayment terms, they can be an ideal solution if you’re in urgent need of funds. The application process typically requires minimal documentation, allowing individuals with varying credit profiles to qualify. For instance, even those who have experienced a bumpy financial road may find themselves eligible for personal loans with higher interest rates.

FastLendGo simplifies the comparison between different lenders by providing transparent information on interest rates and repayment terms, helping borrowers make the best choice suited to their needs.

However, personal loans also come with their share of downsides. High-interest rates are a significant drawback compared to secured loans like home equity loans. While some individuals can secure favorable rates through excellent credit scores or established relationships with lenders, others might find themselves burdened by steep monthly payments and extended repayment periods.

Another notable risk associated with personal loans is the possibility of defaulting on payments due to unforeseen financial setbacks. Defaulting not only damages your credit score but also incurs additional fees and penalties that can compound into a financial nightmare.

Home Equity Loans: Securing Your Future

On the flip side, home equity loans offer substantial borrowing power, making them an attractive option for those with significant home equity or large expenses. Unlike personal loans, which are unsecured, home equity loans use your home as collateral, offering a level of security that lenders find appealing.

One of the most compelling benefits of home equity loans is their lower interest rates compared to personal loans and credit cards. This advantage translates into more affordable monthly payments and reduced overall borrowing costs. For those aiming for long-term financial stability, choosing a home equity loan can be akin to investing in your own future.

However, it’s crucial to weigh the risks associated with home equity loans before making a decision. The primary risk lies in the potential loss of your home if you default on payments. Lenders have the legal right to foreclose on your property should you fail to meet repayment obligations. Additionally, if the real estate market experiences a downturn and your home’s value decreases below what you owe, you could find yourself owing more than the house is worth, complicating any future plans of selling or refinancing.

Choosing Between Personal Loans and Home Equity Loans

When deciding whether to opt for a personal loan or a home equity loan, it’s essential to consider several factors. First and foremost, evaluate your financial stability and creditworthiness. If you have excellent credit, you’re more likely to secure a lower interest rate on a personal loan, making it a potentially less risky option.

However, if you’re looking for larger sums of money or are willing to take on the collateral risk associated with home equity loans, these can be an attractive choice due to their lower interest rates and potential tax benefits. For example, using funds from a home equity loan for qualifying home improvements could provide significant tax deductions at year-end.

Moreover, if you have a considerable amount of equity in your property or are dealing with lower credit scores, home equity loans may offer more favorable terms than personal loans. The flexibility in usage and the potential to secure larger amounts through home equity lines of credit (HELOCs) make them a compelling option for many homeowners.

Comparing Lenders: A Guide to Finding the Best Deal

When shopping around for either type of loan, it’s crucial to compare offers from multiple lenders. Each lender may have different terms, interest rates, and fees that can significantly impact your financial health over time.

A useful tool in this process is FastLendGo’s comprehensive platform, which allows borrowers to compare various loans side by side. By inputting basic personal information such as income, credit score, and desired loan amount, users receive tailored recommendations from top lenders.

Additionally, understanding the fees associated with each loan type can save you significant money. Personal loans often come with origination fees and late payment penalties, while home equity loans may incur closing costs and prepayment penalties. These fees, though seemingly minor, can add up over time and affect your overall borrowing cost.

Considerations for Borrowers: What to Keep in Mind

Before finalizing a loan agreement, consider the long-term implications of your choice. Personal loans are generally unsecured but come with higher interest rates and shorter repayment periods compared to home equity loans. On the other hand, while home equity loans offer lower rates and larger borrowing limits, they require you to put up collateral in the form of your home.

If you’re planning to use the borrowed funds for large purchases or significant investments, such as renovations or paying off high-interest debts, a personal loan might provide better flexibility without risking your property. However, if you’re looking to secure lower rates and larger sums of money, a home equity loan could be more advantageous.

Tips for Navigating the Loan Application Process

Navigating the loan application process can seem daunting but with proper preparation, it becomes much smoother. Start by gathering all necessary documentation such as proof of income, tax returns, and credit reports. This upfront effort not only speeds up the application process but also increases your chances of approval.

For home equity loans, expect a more rigorous evaluation process due to the collateral involved. Lenders will typically require an appraisal to determine the value of your property before extending loan offers. Be prepared for this step as it can add several weeks to the overall timeline.

When applying online through platforms like FastLendGo, ensure you provide accurate and up-to-date information. Misrepresenting details such as income or employment status can lead to denial or higher interest rates. Transparency is key in building trust with lenders and securing favorable terms on your loan.

Final Thoughts

Choosing between a personal loan and a home equity loan involves careful consideration of various factors, including financial stability, creditworthiness, and long-term goals. While both options have their unique advantages, understanding the nuances can help you make an informed decision that aligns with your specific needs.

Whether you’re consolidating debt or financing significant expenses, taking the time to compare lenders and understand the terms of each loan type is crucial for financial success. By leveraging tools like FastLendGo’s platform and staying informed about market trends, borrowers can navigate the complex world of personal finance with confidence and ease.